Amid a moderate global growth clouded by the intensified geopolitical tensions and military conflicts as well as still high interest rates, ASEAN economies continued to remain resilient and delivered credible economic performance in the first three quarters of 2024.

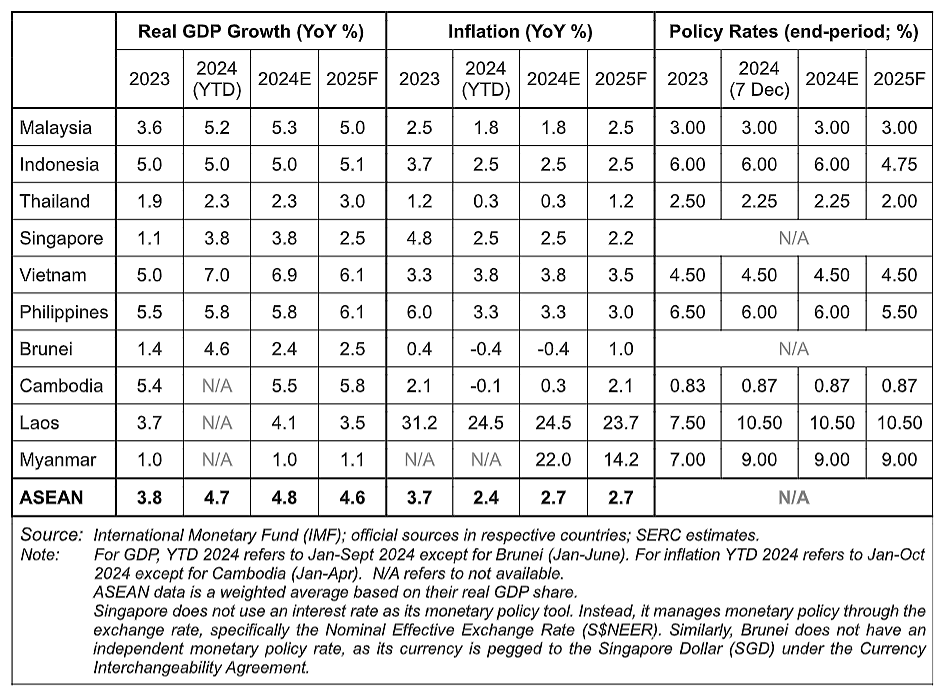

Sustained high real GDP growth was reflected in Malaysia (+5.2 per cent y-o-y in the first nine months of 2024), the Philippines (5.8 per cent), Indonesia (5.0 per cent), Vietnam (7.0 per cent) and Singapore (3.0 per cent).

This was underpinned by supportive fiscal policy and accommodative monetary stance, moderate inflation trajectory and stable labour market conditions.

Growth drivers of ASEAN were driven by resilient domestic spending, albeit slower. It was observed higher gross fixed capital formation in some economies such as Malaysia in the manufacturing, services, telecommunication sectors and data centres well as public investment in transportation, highways and 5G infrastructure.

Public infrastructure spending remains on track in the Philippines. Indonesia’s infrastructure development, including the new capital city Nusantara, presents opportunities for investors in construction, logistics and real estate.

The export-oriented economies have benefited from an improvement in global demand, upturn in global tech cycle and firmer commodity prices.

The tourism industry is on track to its full recovery. While the number of tourists has yet returned to pre-COVID-19 pandemic levels for Malaysia, Indonesia, Vietnam, Singapore and Thailand, international tourism has bounced back to between 66 per cent and 78 per cent of pre-pandemic levels in the first nine and ten months of 2024, with substantial potential ahead.

FDI inflows into ASEAN have remained strong.

For three consecutive years (2021-2023), ASEAN has maintained its position as the top FDI among developing regions with FDI inflows reaching a new historical level of US$231.2 billion in 2023 (US$227.9 billion in 2022 and US$209.8 billion in 2021).

Amongst the top sources of FDI for ASEAN in 2023 were the United States, intra-ASEAN, China, Hong Kong, China, Japan and South Korea.

Based on net FDI inflows in the first half-year and nine months of 2024, it is estimated that net FDI inflows could reach between US$220.0-US$230 billion in 2024.

Investment prospects for ASEAN should remain promising in 2025 and beyond. In an era of potentially more disruptions and uncertainties masked by the shifting global economic dynamics, redirection of investment flows and reconfiguration of supply chains to mitigate the geopolitical risks and potential wider scale of trade and technology-related conflicts between the US and China, ASEAN must enhance its resilience and appeal as a leading destination for FDI.

ASEAN governments have to drive stronger regional integration as it increases opportunities.

The more attractive investment environment, to improve efficiency, to build regional supply chains security and networks, leverage on complementary locational advantages.

Amongst ASEAN economies, Malaysia focuses on high growth high value (HGHV) sectors covering digital and technology-based industries; electrical and electronics; data centres, smart agriculture and agro-based activities; rare earth; and energy transition.

Key areas of opportunities in Indonesia are renewable energy (solar and hydroelectric power), green technology, healthcare, fintech, and digital economy.

Energy, manufacturing, and real estate were the major investment sectors in Vietnam while in the Philippines, the digital economy (fintech, IT, and e-commerce), real estate, infrastructure and renewable energy (such as solar panel manufacturing, wind farm development, and smart grid technologies) some of the most promising industries for investors.

Economic diversification and deepening inter-and intra-ASEAN collaboration and integration would ensure a robust ASEAN economies, placing the region in a better position to withstand disruptions in an increasingly multipolar world.

Most central banks in Interest rate trajectories in ASEAN are diverging when the US Federal Reserve cut its interest for the first time in four years in September 2024.

With inflation pressures cooling off, most central banks in ASEAN economies have cut their interest rates on a measured pace in 2H 2024 as they anchored their domestic-driven economies though the monetary easing are likely to move gradually.

Bank Indonesia, Bank of Thailand, the State Bank of Vietnam, and Bangko Sentral ng Pilipinas lowered their interest rates to hold up the loosening domestic demand in recent months.

The Monetary Authority of Singapore has maintained the prevailing rate of appreciation of the S$NEER policy band until the core inflation is closed to desired levels.

Bank Negara Malaysia, meanwhile, has been holding the policy rate steady to support domestic demand amid steadying inflation.

A number of central banks in ASEAN will continue to cut interest rate in 2025, but will be shallower than that of advanced economies.

The central banks will still be keeping tab on the geopolitical tensions in Ukraine and the Middle East, the monetary stance in advanced economies as well as global commodities and energy markets.

For 2025, ASEAN economies are projected to sustain steady growth trajectory, albeit unevenly, with the region’s real GDP growth to expand by 4.3 per cent compared to estimated 4.7 per cent in 2024.

The 2025 growth projection is premised on continued domestic demand and easier financial conditions on lower interest rates and ample liquidity.

However, we caution that the strength of external demand for most ASEAN economies will be impacted at varying degree by President Trump’s tariffs threat and domestic tax incentives policy to encourage reshoring of the US companies and investments back to the US.

These protected policies are expected to disrupt the trade and investment flows into emerging markets, including ASEAN.

Besides specifically targeting imports from China with the imposition tariffs as high as 60 per cent, Trump also signalled the intentions to impose potential tariffs of 10 to 20 per cent on imports from other countries.

As ASEAN is the fourth-largest trading partner of the US, exporting a range of raw materials and assemble goods, including electronic components, apparel, footwear, and tires, while importing products such as electrical machinery, petroleum oils, soybeans, and aircraft.

The proposed increase in tariffs would make ASEAN goods less competitive in the US market.

If the US manufacturing reshores, induced by lower corporate tax rate as promised by Trump, it could reduce demand for ASEAN’s manufacturing output, impacting the ASEAN suppliers’ networks, production and exports.

The potential impacted industries could be textiles, semiconductors, telecommunications, electrical equipment, machinery, computers, and automotive industries.

However, ASEAN remains a hot spot for investment in the global economy given its diverse economic structures, demographic dividend and a large domestic market, and strategic position as attractive manufacturing hub as well as the region’s integration with global supply chains.

During the first-term presidency of Donald Trump, US-China trade tensions have caused trade diversion and the part relocation of production operation in China to nearby countries, benefitting ASEAN countries under a “China Plus One” strategy.

Trump 2.0 will inevitably impact on ASEAN, though the direct and indirect effects can be partially mitigated by resilient domestic demand.

ASEAN must continue its economic diversification, deepen regional cooperation and economic partnerships, strengthen supply chains and expanding trade ties through ASEAN-China Free Trade Area (ACFTA), Regional Comprehensive Economic Partnership (RCEP), and the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP).

Additionally, ASEAN businesses must proactively engage in forging strategic partnership and business-business relations with non-traditional countries to mitigate the risks induced by the US economic policy.

In conclusion, economic diversification and deepening inter-and intra-ASEAN collaboration and integration would ensure a robust ASEAN economies, placing the region in a better position to withstand disruptions in an increasingly multipolar world.

(Lee Heng Guie, Executive Director of Socio-Economic Research Center (SERC), the Associated Chinese Chamber of Commerce and Industry Malaysia, ACCCIM.)

ADVERTISEMENT

ADVERTISEMENT